A customer pulls out a smartphone to pay at a small neighborhood shop in Lahore, Pakistan. The shopkeeper shakes their head and points to a faded "Cash Only" sign. This scene plays out thousands of times daily across Pakistan, even though both parties likely have digital wallets. Digital payment systems are expanding rapidly in Pakistan, but cash still dominates retail transactions. In 2024, only 4.3 percent of individuals paid a merchant digitally. Pakistan has over 4 million micro, small, and medium enterprises. The government launched RAAST, its interoperable instant payment system, in 2022. Yet in most small retail shops, cash remains the dominant payment method. The infrastructure exists, and the technology works, so why are people not using it?

A research team from Lahore University of Management Sciences, the University of Sydney, and the College of William and Mary set out to answer that question. They aimed to understand why both merchants and households resist using digital payments and whether misconceptions around digitization are a driving factor. The researchers conducted baseline surveys with 1,192 (micro and small) merchants located in 279 markets in peri-urban areas of three districts in Punjab, and 1,189 households living near these markets. The study focuses on a deliberately selected setting where basic access constraints are largely absent.

Digital access is high, but adoption of digital payments remains limited

All merchants in the sample can receive or make digital payments;

- around 90 percent report access to a smartphone

- an estimated 70 percent have access to the internet.

Among households,

- approximately 80 percent have a smartphone,

- close to 97 percent report that they or someone in their household has a digital financial account.

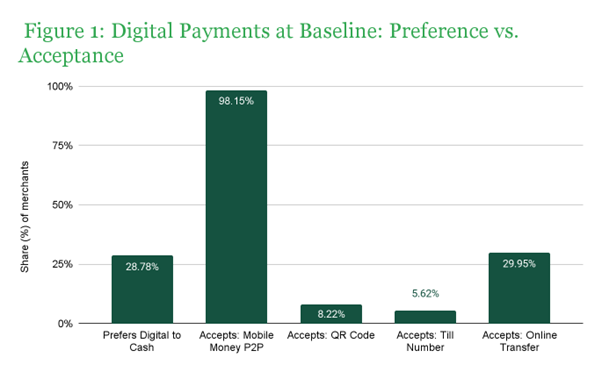

Yet, the actual use of digital payments at the point of sale remains low. Nearly two-thirds rank cash above any digital means of transactions, including mobile money, QR code, merchant tills, and online banking transfers. While almost all merchants accept at least one form of digital payment, acceptance is heavily concentrated in specific methods: peer-to-peer mobile money transfers are most accepted, while fewer than 10 percent of merchants report accepting QR code-based person-to-merchant (P2M) payments, and only around 30 percent prefer digital payments over cash for routine transactions (Figure 1).

Fraud and reliability concerns dominate stated barriers

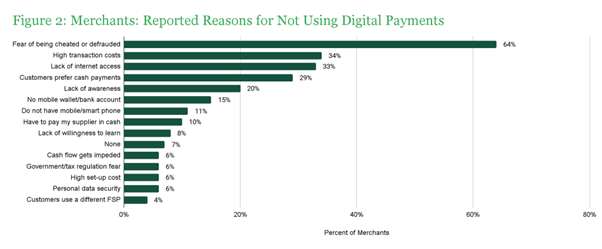

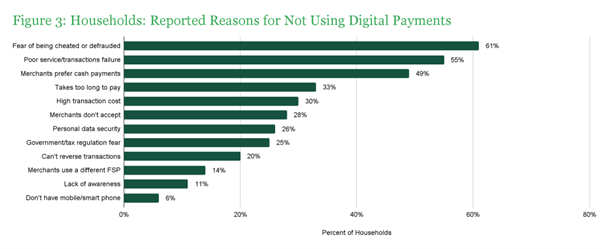

To understand why usage remains low despite high access, merchants and households were asked directly about their reasons for not using digital payments more frequently. The top concerns for both groups included fraud and transaction reliability. Merchants most commonly cited fear of being cheated or defrauded, followed by high transaction costs, connectivity issues, and concerns that customers prefer cash. Households reported similar concerns, including fear of fraud, failed transactions, difficulty reversing payments, and data security risks (Figure 2).

In reality, while 68 percent of merchants experienced at least one negative outcome when using digital payments, only 14 percent classified these experiences as fraud, though 30 percent reported knowing others who had experienced fraud directly. Merchants tend to define “fraud” broadly, focusing on failed or reversed transactions and dispute resolution, and noted that safety improvements should prioritize dispute resolution mechanisms. Taken together, these findings underscore how important reliability and recourse are to merchants, while also revealing that fraud is not nearly as prevalent as they perceive it to be.

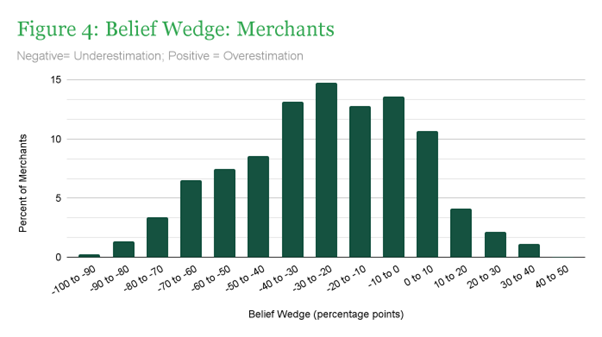

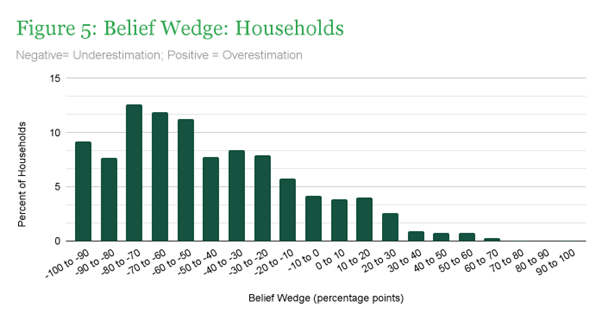

Misperceptions may further inhibit coordinated adoption

The data reveals something else: a critical misperception that may be holding everyone back. The researchers call this a “belief wedge”—the gap between what people think others prefer and what others actually prefer. Merchants tend to underestimate how many of their customers value digital payments, while households underestimate how many merchants are willing to accept them (Figure 3). This matters because digital payments require coordination. Even when concerns about fraud and other risks are real, these misperceptions may create additional barriers by slowing a coordinated shift away from cash.

Note: A “wedge” is the gap between what people think others want and what they actually want. A negative wedge means merchants (or households) underestimate how much others in their area are interested in using digital payments. Very large gaps (below -100 percentage points), which make up about 5% of responses, are grouped together for readability.

The baseline evidence suggests that low digital payment adoption in Pakistan is not about access or perceived value. The infrastructure exists, people understand how it works, and many see its benefits. Instead, adoption appears to be associated with two key factors: perceived risk from negative experiences, and coordination frictions rooted in misperceptions about others' preferences. Without correcting these barriers, cash will likely continue to dominate regardless of how sophisticated the payment systems become.