Abstract

Digital tools have enabled people around the world to access banking and financial services. The rise of these technologies, however, has been accompanied by an increase in fraud risks, which are often difficult to measure due to consumer underreporting or unawareness. In Kenya, researchers conducted a research project to measure individuals’ level of scam identification ability, asking participants to classify example messages as fraudulent or genuine. Additionally, the researchers tested whether providing information about common features of SMS scams could help consumers classify the messages. The results revealed that only two percent of respondents correctly classified all messages. Providing information did not significantly improve respondents’ ability to identify scams.

Policy Issue

The use of digital tools has successfully expanded access to banking and financial services in many developing countries. However, with this expansion there has also been an increase in many issues related to consumer protection, in particular fraud.[1] Fraud threatens both consumer welfare and trust in the financial services market. As digital fraud in developing countries is still a fairly new issue, research in this area has been largely focused on curbing agent misconduct even though fraud can manifest in various forms. In particular, SMS and phone scams are increasingly popular channels for fraud.

Understanding the prevalence of fraud can be challenging because consumers underreport fraud or might not recognize whether they have been contacted by a scammer. IPA's evidence suggests that while fraudsters target all demographics of victims (through dialing random numbers), 68 percent of respondents with a tertiary education reported scam events (as compared to 50 percent of respondents with a secondary school education or lower). This suggests that education levels may affect consumers’ ability to identify and/or report scams. As such, concerted efforts taken to increase consumers’ ability to identify scams and confidence to report scams can potentially help policymakers understand the scope and nature of fraud.

Context of the Evaluation

Kenya is a global leader in digital financial services usage with 79 percent of adults using mobile money in 2019. Despite widespread use, a recent phone survey conducted by IPA revealed that 56 percent of respondents in Kenya reported having faced phishing attempts via phone call or SMS. Yet, consumers are not likely to use formal complaints channels. When they do use these channels, consumers are unlikely to receive a prompt and effective resolution.

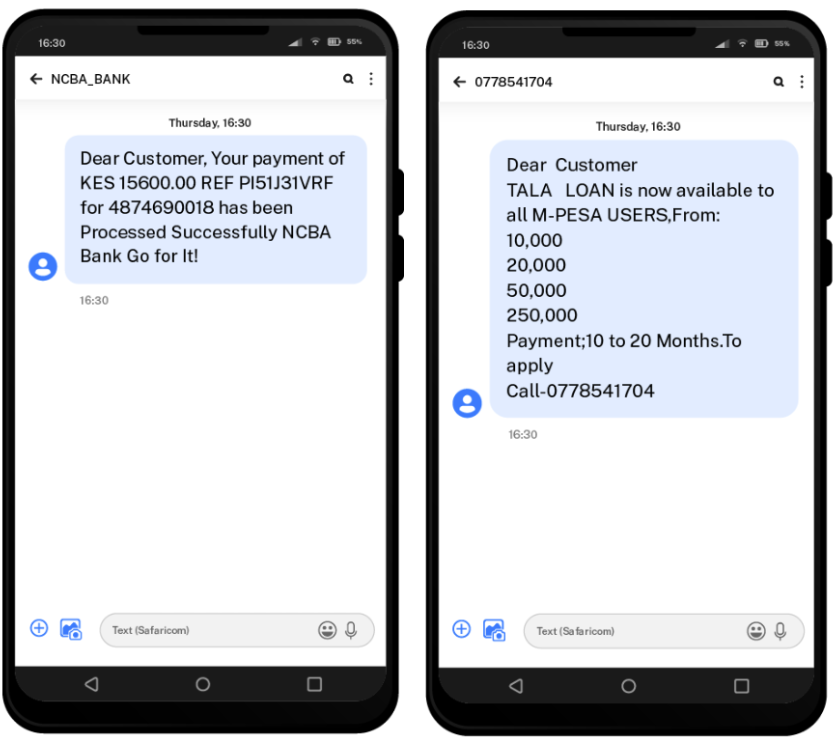

Details of the Intervention

In Kenya, researchers conducted a research project to measure whether the provision of information about common features of fraudulent messages could help users correctly identify scams. The research comprises three main activities:

- Social media data collection and analysis: Researchers collected and analyzed data from 18,000 public posts on Facebook and 427,000 on Twitter that contained at least one scam-related keyword and were sent from Kenya. Topic clustering revealed common types of scams discussed on social media.

- Qualitative interviews and focus groups: Researchers conducted five focus group sessions to qualitatively understand the scope of scams faced by consumers. Qualitative interviews with various stakeholders of the supply side of digital financial services complemented the views of consumers.

- Online survey: Researchers conducted an online survey with 1,000 individuals in Kenya. Respondents were presented 12 images of messages and asked to classify them as either “scam” or “not scam”. These images were selected from the social media scraping exercise as described above in Activity 1. Researchers randomly provided half of the sample with tips on how to spot scams.

Results and Policy Lessons

The results suggest that providing information may not be a viable solution to mitigate vulnerability to scams. Therefore, untargeted information campaigns may not be a cost-effective policy effort.

Mobile phone scams were diverse. The social media data analysis revealed scam messages may talk about winning a price, an erroneous financial transfer, potential job offers, loans, and other topics. The sender often pretended to be a telecom company, a bank, or a friend.

Fraudsters posed as trusted individuals. In line with the social media analysis, the qualitative interviews revealed that fraudsters often impersonated agents, family or friends. The goals of phone scammers were diverse: obtain money, personal details, and/or perform identity theft.

Consumer awareness of phone scams was mixed. The qualitative interviews suggest that active digital financial services (DFS) users are more aware of scammers’ tricks than non-active and non-user segments. The youth and the elderly, women and rural populations were perceived to be especially vulnerable. This is partly confirmed in the online survey, where women and less frequent users of DFS performed worse in terms of scam classification.

Out of the 12 messages that researchers showed survey respondents, 8.6 were correctly identified, on average. Respondents were slightly better in identifying scams (73 percent correct as compared to 67 percent correctly identified official messages). However, only two percent of respondents identified all 12 messages correctly.

Information did not improve scam identification ability on average, but it increased average confidence. Survey respondents in the treatment group received information on how to spot scams after six messages were shown. Individuals were not likely to improve their classification for the second six messages as compared to the control group, which did not receive information. But information appeared to make respondents more likely to classify a given message as scam, i.e., respondents became more cautious. In addition, respondents who received information had higher confidence in their classification.

Sources

[1] Joseck Luminzu Mudiri. “Fraud in Mobile Financial Services” https://www.microsave.net/files/pdf/RP151_Fraud_in_Mobile_Financial_Services_JMudiri.pdf