![]()

Since its introduction in 2020, Pix, Brazil’s1 instant payment platform, has transformed the country’s payment landscape, rapidly digitizing transactions and fundamentally changing how small businesses operate. In our earlier work with micro and small enterprise (MSE) owners, we found that they have not only embraced Pix at remarkable rates, but are also highly digitally and financially literate. Pix has successfully enabled millions of small businesses to participate in the digital economy. This raises a new set of questions: What role do these instant payment systems play in increasing overall financial inclusion and trust in financial systems? Can they expand access to other beneficial financial products and services, such as Open Finance?

Between April and July of 2025, we surveyed 1,151 MSE owners in Espírito Santo to understand how Pix is influencing the adoption of Open Finance. Open Finance allows individuals and businesses to securely share a range of data points, such as payments, investments, and insurance, across institutions. Beyond mapping current usage patterns, we also tested whether a targeted information intervention could encourage business owners to adopt Open Finance.

Pix Dominates Small Business Payments, but Mostly Off the Books

Consistent with our earlier pilot results, our survey found that Pix usage is nearly universal among the small business owners in our sample. At baseline, 97 percent of firms use Pix. The majority of firms use Pix daily for both business and personal transactions. On average, these transactions account for nearly 90 percent of all non-cash business revenues.2 However, the majority of these transactions flow through their personal accounts, which may limit their business’s eligibility to access products designed specifically for businesses.

Open Finance Adoption by Business Lags

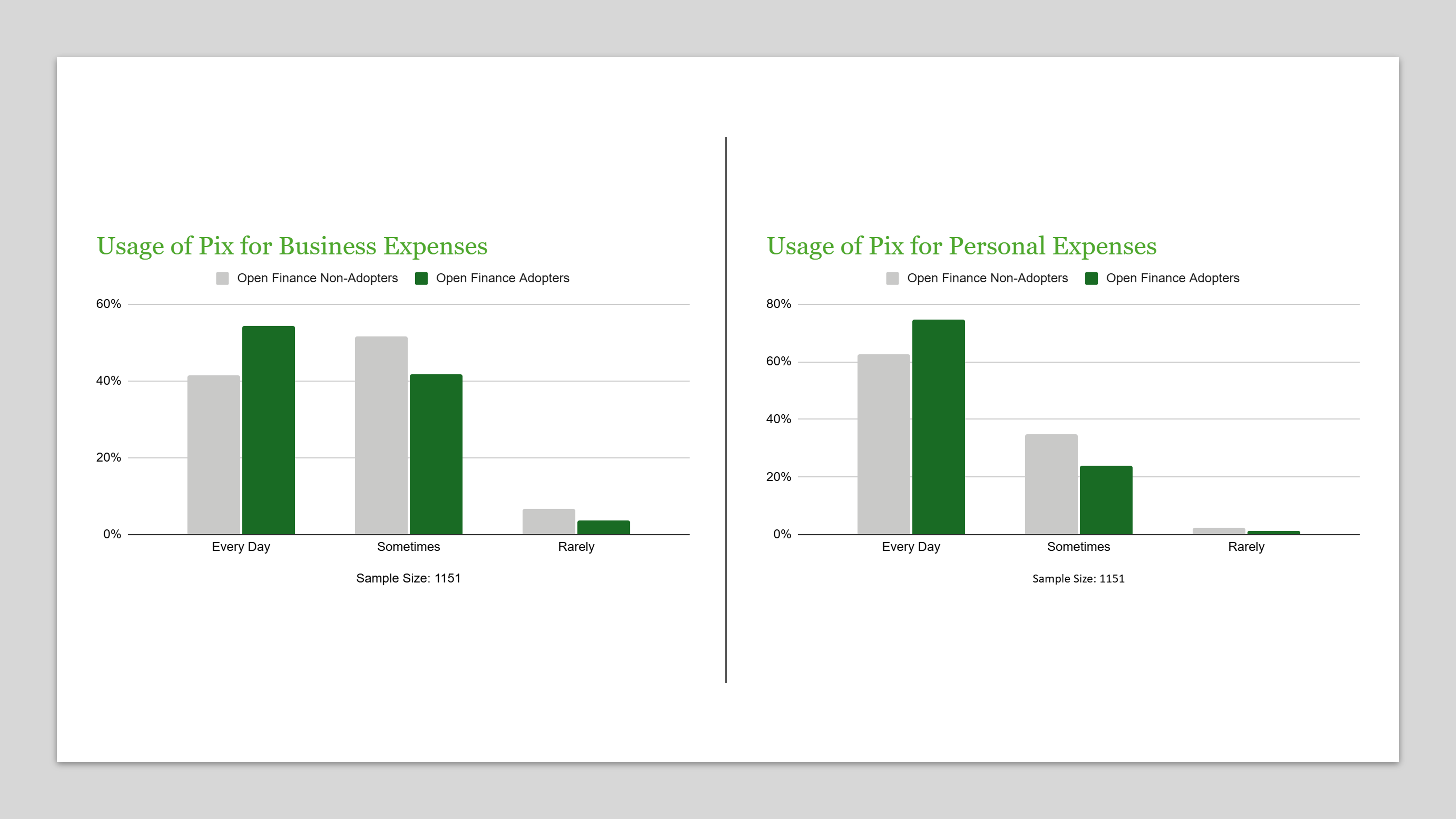

Open Finance became available to small business owners in early 2021. Although adoption by individuals has been noteworthy, adoption by firms has been lagging behind, with less than 3.2 percent of Brazilian firms having adopted Open Finance as of July 2025.3 Findings from our work broadly align with these estimates. Before our program, about 10 percent of firms surveyed knew what Open Finance was, and fewer than 8 percent had enrolled. Yet we also observed a clear pattern: firms that use Pix more frequently, whether through personal or business accounts, were significantly more likely to have adopted Open Finance (see Figure 1).

Figure 1: Usage of Pix for personal and business expenses and Open Finance adoption

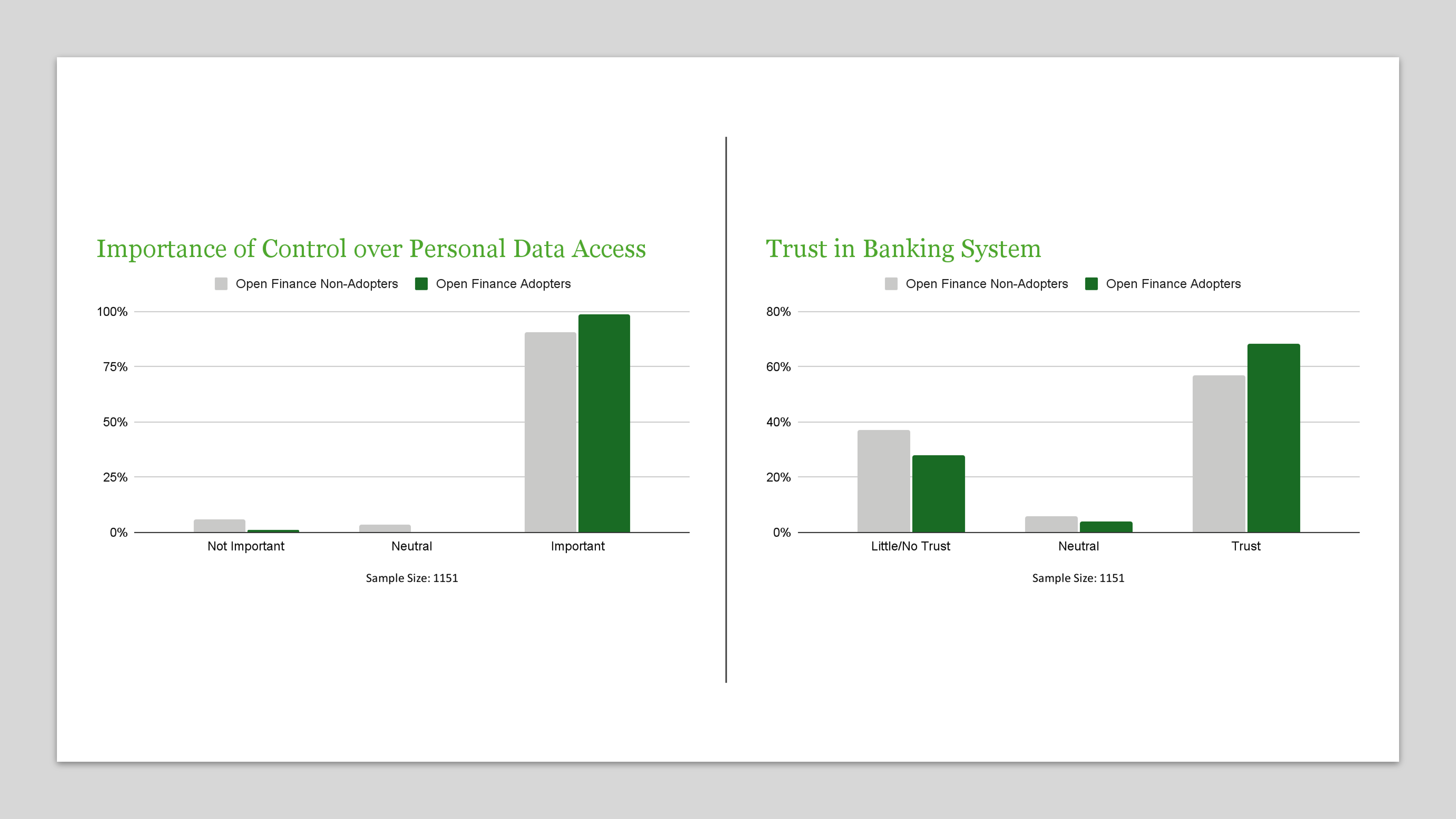

Additionally, we find that more digitally savvy firms – those that use digital or app-based systems for managing inventory – are also more likely to have adopted Open Finance. Rather than simply reflecting technological capacity, this pattern suggests a behavioral dimension. To better understand this, we asked respondents about the importance of control over their personal data access (see Panel A Figure 2) and their trust in the banking system (see Panel B Figure 2). We found that adopters report both higher trust in the banking system and a stronger sense of the importance of aving control over their financial data.

Figure 2: Importance of data control, trust in the banking system, and Open Finance adoption

These patterns suggest that digital saviness, trust, and perceived control play an important role in Open Finance adoption. However, low awareness and adoption rates highlight the need to identify and test effective strategies for increasing participation.

Facilitating Adoption: A Randomized Evaluation

Based on these insights, our team conducted a randomized evaluation with the 1,151 business owners to test whether providing information about the policy and the enrollment process for Open Finance could increase participation. We divided participants into two groups: one that watched a 3-minute-long video introducing them to Open Finance and how to enroll, called the ‘programmatic group’, and the other, which watched a different generic video about financial inclusion, called the comparison group. We then used follow-up surveys to determine if people’s thoughts and behaviors towards Open Finance changed.

Figure 3. Screenshot of Video

Information Moves the Needle

Following up with firms two weeks after the video, we found that approximately 26 percent of programmatic firms signed up, as compared to only 17 percent of the comparison firms, showing more than a 40 percent increase in adoption by the programmatic group.

Digital Readiness and Financial Evolution

Pix has not only made payments faster and cheaper, but it can also be a powerful catalyst for deeper financial participation. Yet, we also find that this participation, including the adoption of Open Finance, may depend on more than access to digital tools. Building trust in financial systems and data-sharing platforms could also be pivotal, particularly among informal or cash-heavy firms, which may have less experience with Pix.

Our findings suggest that the next stage of digital inclusion will depend not only on technological access but also on the institutional trust and behavioral confidence to enable deeper financial engagement.

Our next blog will dig deeper into learnings on the impact of open finance on small business credit access, amongst other outcomes on their financial health.

Stay tuned!

1The views expressed in this blog post are those of the authors and do not necessarily reflect those of the Banco Central do Brasil.

2Data on non-cash revenue comes from the Central Bank, and the Bank does not report on cash usage. However, our primary data show that approximately 60% of firms receive at least 80% of their payments in non-cash.

3This is based on the Open Finance Brazil, which reports the number of consents received from individuals (63 million) and firms (771 thousand). Since an individual/firm can initiate multiple consents, we cannot determine the number of unique adopters, but we can estimate a maximum. Our ceiling – 30 percent for individuals and 3.2 percent for firms – is based on the total population of Brazil (212 million) and the total number of firms (24 million).