Imagine your phone buzzes with a text message claiming you've won a prize. All you need to do is send a small "processing fee" to claim it. Or you receive a call from someone claiming to be a customs official, demanding payment to release a package in your name.

These aren't just hypothetical situations—they're happening right now across Africa.

In Uganda, one in three mobile money users reported being targeted by fraudsters in 2020. The numbers are even higher in Kenya and Nigeria. Consequently, millions of users in Uganda – and millions across Africa – have lost money to fraudsters who use mobile money as their channel for deception. This creates real economic harm and reduces trust in formal financial services.

Preventing Fraud in Digital Financial Systems

To protect themselves from mobile money fraud, consumers need the right information, in the right format, at the right time. For rural and low literacy populations, circulating written information or videos on social media may not work. However, in our experience technology can help overcome these communication challenges. In a recent study in Uganda, IPA partnered with Viamo, a digital education provider to develop a series of interactive, story-based fraud prevention audio lessons in which users listened as fictional consumers interacted with fraudsters who were trying to deceive them. Branded as “Beera Mubangule” or “Be Aware,” the stories were delivered through interactive voice response (IVR) games, which did not require listeners to be literate or have a smartphone since the technology worked on even the most basic mobile phone.

They listen to realistic scenarios where fictional consumers interacted with fraudsters attempting a common scam, like in this story

At critical moments, users make choices about how to respond

The story adapts based on their decisions, teaching them the consequences of different actions

Check it out for yourself here:

Stop, Check, Act

After interviewing real fraud victims, we identified common tactics: fraudsters create false urgency, discourage reflection, and prevent consultation with others. We designed the IVR stories to convey a simple metaphor: Preventing fraud is like crossing the street – you should “Stop, Check, Act”:

Stop - gain awareness of the risk and disengage the caller,

Check - consult people or sources you trust,

Act - take appropriate action, such as reporting the phone number if it is indeed a fraudster.

As a result, IVR content participants experienced the following effects, all of which are statistically significant:

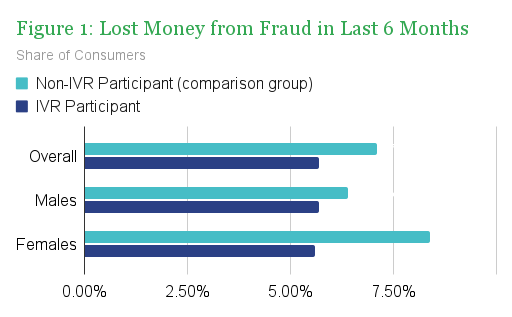

Fewer instances of fraud victimization. The percentage of consumers who reported losing money from fraud reduced from 7.1 to 5.7 percent in the previous six months, including a reduction from 8.3 to 5.7 percent for women (figure 1).

More fraud reporting. Two of three people in the sample experienced a fraud attempt in the previous six months, but those in the treatment group were 50% more likely to report the incident (35.6 percent of the treatment compared to 23.2 percent of the control). Reporting fraud attempts to formal channels is key to identifying fraudulent actors and shutting down their accounts before they can harm others.

More use of complaints systems. Overall, the likelihood of having made a formal complaint of any type increased by 32% (from 18.7 for the control to 24.7 percent for the treatment). Even though the content focused only on fraud, it encouraged more generalized use of consumer redress systems.

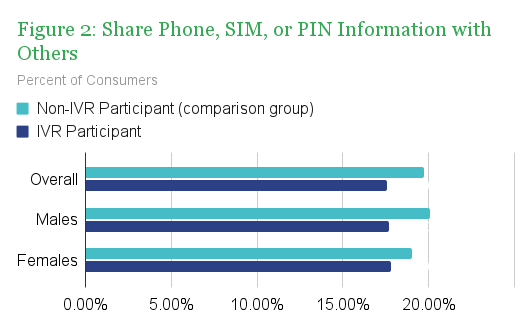

Less PIN sharing. The percentage of people sharing their phone, SIM, or pin information with others decreased from 19.7 to 17.6 percent (Figure 2). Sharing this information increases the risk of fraud by making it more likely someone will access your account without your permission.

More checks for fraudulent SIM registrations. The number of respondents who checked if there are SIM cards registered with their national ID that they don’t know about increased from 21.2 to 24.9 percent, using the Uganda Communications Commission’s free SIM registration check shortcode. This helps root out fraudsters who use accounts in others' names to target their victims.

There was an increase in the use of mobile money for savings, from 37 to 39.9 percent, indicating that increased fraud awareness did not reduce trust in mobile money.

There has been an increase in the use of mobile loans among women, from 21.2 to 24.1 percent, helping to address the existing credit gender gap in Uganda.

The interactive “choose your own adventure” approach to the narrative content also made it engaging for the users. In our main fraud game, 93 percent of learners who started the game completed both levels, and 58 percent of these learners repeated the game more than once. This is notable since users took an average of 18 minutes to complete the game. The IVR-based content was also low-cost, so scaling up this content nationally would have very small incremental costs (nearly zero per additional user assuming zero-rating of SMS and voice costs by mobile network operators or MNOs), and is far less expensive than other anti-fraud media campaigns currently used in Uganda such as in-person workshops.

What next? Scaling Across Africa

Overall, the results from the pilot indicate that simple, action-oriented, and localized IVR-based content can reduce fraud victimization, improve consumer protection knowledge and practices, and potentially improve usage of digital financial services.

If we scale up the IVR content to 1 million mobile money users, for example, with the same 1.4 percent reduction in fraud victimization, it could mean 14,000 fewer fraud victims and USD 546,000 less in losses from fraud. This reduction in fraud losses would far exceed the costs of delivering 1 million additional IVR sessions. The incremental costs are minimal and testing and content development costs were less than USD 150,000. Because Viamo has IVR platforms in over 20 digital financial services markets, the content could be expanded across countries simply by translating and contextualizing the content used in Uganda.

In fact, the larger the number of users, the better the cost-benefit for fraud prevention via IVR. When we remember that there are tens of millions of mobile money customers in Uganda, and more than 800 million registered mobile money accounts across sub-Saharan Africa, the potential to help protect users from fraud through IVR expands even further. The positive impacts we saw in Uganda are just the beginning of a new approach to fraud prevention content that is low-cost and can reach even the most remote and low-literacy mobile money users. As fraud methods become ever more sophisticated, we need to keep developing new channels and content to help keep consumers safe in digital finance.

Double your impact by becoming a recurring supporter today

For a limited time, a generous anonymous donor will match first-time monthly donations up to $50K. Start a monthly plan today to double your impact while helping provide steady, sustainable support to IPA.