More than three in four adults in Tanzania own a mobile money account. Yet most use it for exactly one thing: cashing money out. Merchant payments account for just 3.9 percent of digital transactions in the country. Utility bills paid by phone sit at 22.7 percent. For the majority of users, mobile money is a corridor rather than a destination — funds move through it on the way back to cash.

The benefits we most commonly attribute to digital financial services (DFS)—reduced poverty, greater financial resilience, broader access to credit—all depend on people using DFS consistently and across a range of transactions. Therefore, an account that exists primarily as a cash-out mechanism delivers little of that promise. So what is keeping Tanzania, a country with mature mobile money infrastructure and an instant payment system, stuck in this pattern?

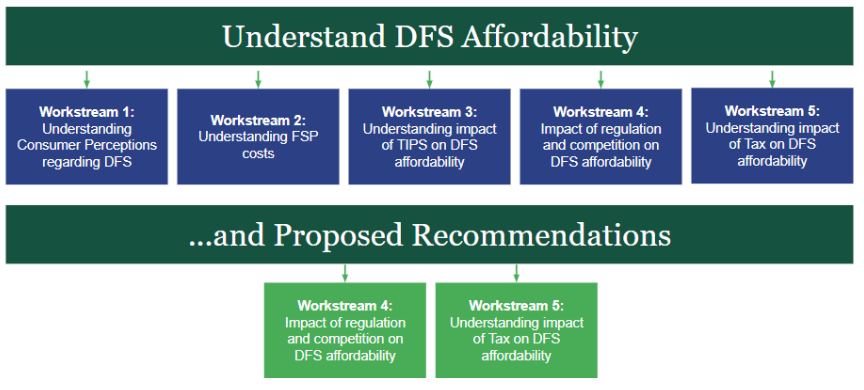

One important contributor is cost. That is what motivated the Tanzania Affordable Digital Finance Research Initiative (TADFRI), a two-year research program developed by Innovations for Poverty Action (IPA) in partnership with the Bank of Tanzania (BoT) and delivered in consultation with Financial Sector Deepening Tanzania (FSDT). The long answer, however, is that costs in a digital payments ecosystem are shaped by multiple intersecting drivers, which a single line of investigation cannot capture. These include consumer behavior, provider economics, market competition, infrastructure design, and tax policy. That is why TADFRI was structured as five distinct research projects. Each project was designed to understand a different aspect of the digital finance ecosystem and how each contributes to the pricing of DFS. Each was led by a specialist team—economists, competition experts, tax consultants, and field researchers — and where data was available, a separate set of findings and recommendations was produced.

Why five projects?

DFS affordability is a systems problem. Consumers who find digital payments too expensive may be responding to transaction fees, layered taxes, misperceptions about cost, or some combination of all three. Providers that set high fees may be managing liquidity, responding to limited competition, or passing through tax burdens to end users. Addressing any one factor without the others produces incomplete solutions, and short-term gains may leave deeper structural problems intact.

What each project found

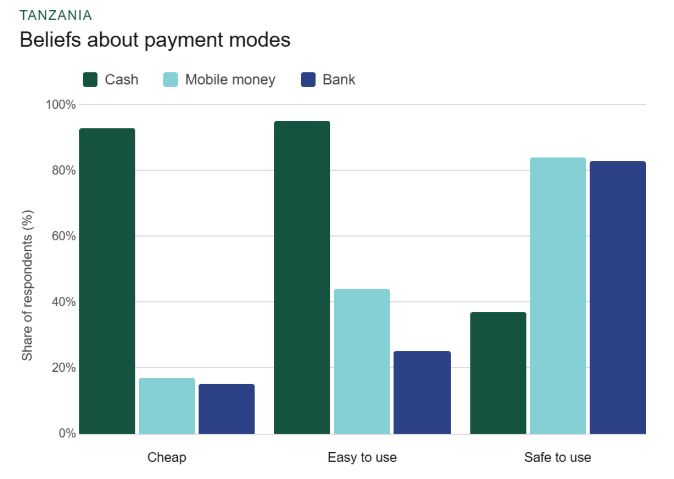

First, we looked at consumers. In a survey of 1,415 individuals who had a mobile money account across Tanzania, more than half underestimated the actual cost of a cash-out transaction. Respondents consistently rated cash as cheaper and easier to use than mobile money, despite cash-out fees regularly exceeding the cost of a direct person-to-person (P2P) transfer. The finding points to something more fundamental than a pricing problem: if consumers do not know what digital payments actually cost, they cannot make informed decisions about when to use them. Pricing transparency plays an important role in enabling users to make informed decisions about different types of transactions. The full findings are available here.

Next, we turned to the supply side, examining agent network costs. Liquidity management — keeping agents stocked with enough float to serve customers — is among the largest operating cost categories for DFS providers, and agents with liquidity issues hit hardest in underserved areas. The research team found that most agents already maintain the relationships and geographic proximity needed to trade liquidity with one another. The main barrier is the lack of a formal architecture to do that. Allowing agent level interoperability could meaningfully reduce a significant cost driver without requiring new infrastructure. The findings from this study will be published on the IPA website in the coming months.

The third workstream examined the Tanzania Instant Payment System (TIPS), and its potential to reshape market dynamics. Interviews with eight financial service providers found that TIPS had already begun to change the competitive landscape. Off-net P2P volume has grown by roughly 18 percent on average on an annual basis between 2022 and 2024, after the soft launch of TIPS in January 2021.1 Banks are increasingly moving into the merchant space, with new strategies to acquire merchants such as provision of working capital, cash flow analytics, and integrated financial solutions. That said, most providers shared that economies of scale from TIPS are yet to be achieved, and without this advantage, cost savings will remain negligible. Details here.

The fourth workstream examined competition and regulation. Tanzania's mobile money market remains highly concentrated and pricing data shows that three major providers have near-identical fees across most transaction bands. The gap between EMI-registered merchants (over 68,000) and bank-registered merchants (roughly 5,500) reflects a structural advantage that compounds over time. Access to USSD infrastructure, critical given that smartphones account for only 32 percent of connected devices, emerged as a bottleneck warranting closer regulatory attention. The workstream 4 policy brief sets out a full set of competition recommendations.

The fifth workstream investigated DFS taxation, which proved to be among the most consequential topics in the research program. Tanzania's current framework layers excise duty, VAT, and a transaction-based levy on provider fees. The research did not find a case for eliminating DFS taxes, but it found a strong case for designing them more carefully, with tiered protections for small-value transactions, phased implementation to avoid trust shocks, and real-time data systems to monitor behavioral responses. Three policy paths are available to Tanzania, and the tradeoffs between them are set out in the accompanying reports.

What the pieces reveal together

Tanzania's DFS ecosystem has the infrastructure to deliver sustainable financial inclusion, but it is held back by a lack of coordination and diverging incentives between providers and the government.

Consumer misperceptions about price have the potential to reduce demand for digital payments. Concentrated market structure reduces provider incentives to compete on price. Liquidity constraints raise costs for agents and limit access in underserved areas. A nascent instant payment system limits competitive pressure from new entrants. And a tax framework deters users it most needs to reach. None of these problems are the cause of high costs alone – they’re all interconnected.

The evidence gathered through TADFRI provides the foundation to understand the drivers of DFS costs holistically. Building on this evidence for concerted action is important and an opportunity that should not be missed.

Sources

1. BoT Aggregate Data, Accessed November 2026